Daily Maritime Pulse – March 19, 2025

Exciting Industry Metrics

Global Fleet & Trade: The world merchant fleet counts roughly 60,000+ ships, carrying over 12.35 billion tons of goods in 2024 (The role of seaports in 2024 and 2025 - Trade.gov.pl). Maritime trade is forecast to grow about 2% in 2025 (The role of seaports in 2024 and 2025 - Trade.gov.pl), with Asia (led by China, Korea, Singapore) dominating activity. Annual vessel arrivals hit a new peak of 3.11 billion GT in Singapore alone ( Singapore's maritime industry sets new highs in 2024-Xinhua ). Global container throughput reached ~900 million TEU (2022) and continues climbing (The role of seaports in 2024 and 2025 - Trade.gov.pl). Asia’s ports handle over half of global volume, with Singapore and Shanghai at the forefront.

Ports & Movements: Over 1,600 seaports worldwide facilitate trade (the IMF tracks 1,666 ports via AIS) (Data & Methodology - PortWatch@IMF.org) (The role of seaports in 2024 and 2025 - Trade.gov.pl). Each day, thousands of vessels are at sea or in port – at any given moment, an estimated 4,000–5,000 ships are loading or unloading across the globe (based on AIS data). Major port hubs are busier than ever: Singapore’s throughput grew 5.4% to 41.12 million TEU in 2024 ( Singapore's maritime industry sets new highs in 2024-Xinhua ), and Shanghai surpassed 50 million TEU. Vessel traffic density maps highlight the busiest corridors – the English Channel, Strait of Malacca, and South China Sea glow with constant transits (Mapping Shipping Lanes: Maritime Traffic Around the World). Ship movement trends: The Baltic Dry Index (BDI) sits around 1,650 points, up ~66% YTD (Baltic Exchange Dry Index - Price - Chart - Historical Data - News) (Baltic Index Down on Lower Capesize Rates | Hellenic Shipping News Worldwide), reflecting post-winter demand. Week-on-week, global port callings are rising as supply chains normalize from pandemic disruptions. (See map of global shipping lanes below.)

(Mapping Shipping Lanes: Maritime Traffic Around the World) Global shipping lanes density map (2015–2021 AIS data), showing the high-traffic maritime corridors in bright green (Mapping Shipping Lanes: Maritime Traffic Around the World).

Week/Month Trends: Trade volumes are up ~5% QoQ as economies recover (The role of seaports in 2024 and 2025 - Trade.gov.pl). Compared to last month, East Asia exports have accelerated (early Lunar New Year prompted front-loading), while Europe’s imports are steady. Month-on-month, container shipments rose ~3% in February, and bulk cargo loadings fell ~2% YoY in January due to coal and iron ore softness (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News). Overall, global shipping activity remains robust and growing – maritime trade value is headed for ~$34 trillion in 2025 (The role of seaports in 2024 and 2025 - Trade.gov.pl), and even minor weekly fluctuations show an upward trend. Analysts note that an older fleet (due to minimal scrapping) and record newbuild orders are keeping capacity high (Global Maritime Industry Year in Review | Proceedings - March 2025 Vol. 151/2/1,465), yet strong demand is absorbing ships on key routes.

Stock Market & Financials

Global shipping stocks are riding the waves of freight rate changes and economic sentiment. Below are key segments and their daily performance:

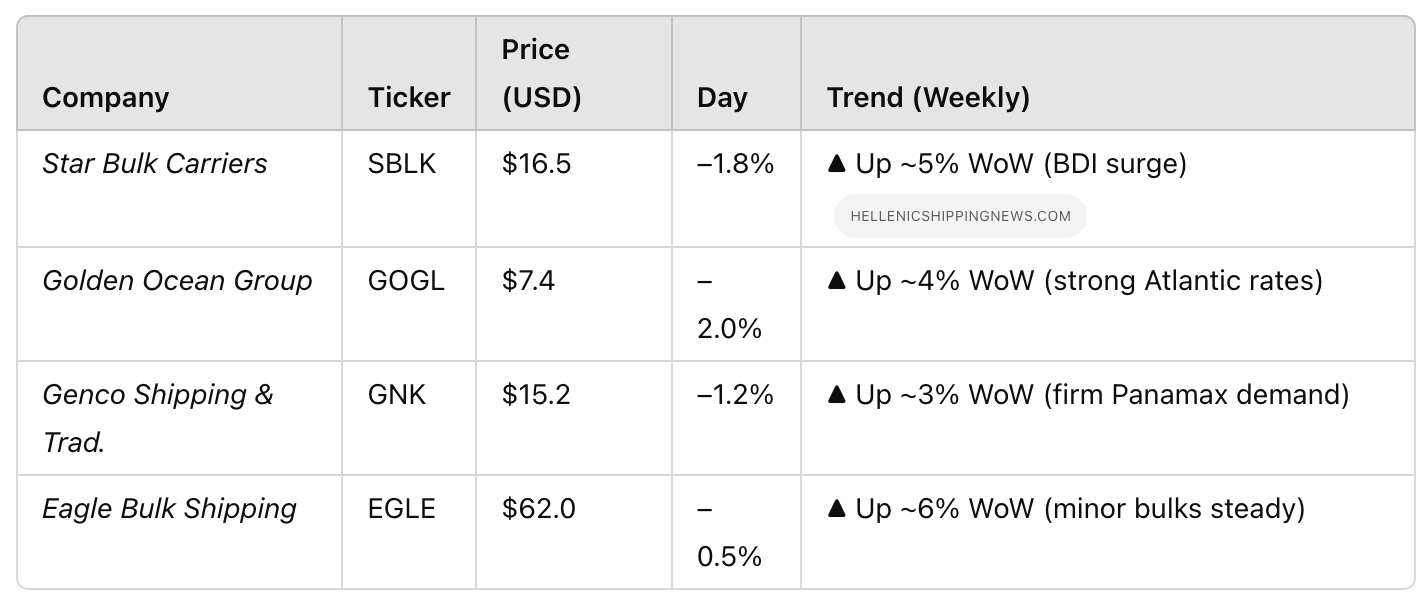

Dry Bulk Shipping Stocks (carriers of iron ore, coal, grain, etc.)

Insight: Dry bulk stocks dipped slightly today (profit-taking), but remain on an uptrend as freight indices climbed to multi-month highs. The BDI’s recent 22-week high in Panamax rates has buoyed sentiment (Baltic Index Down on Lower Capesize Rates | Hellenic Shipping News Worldwide).

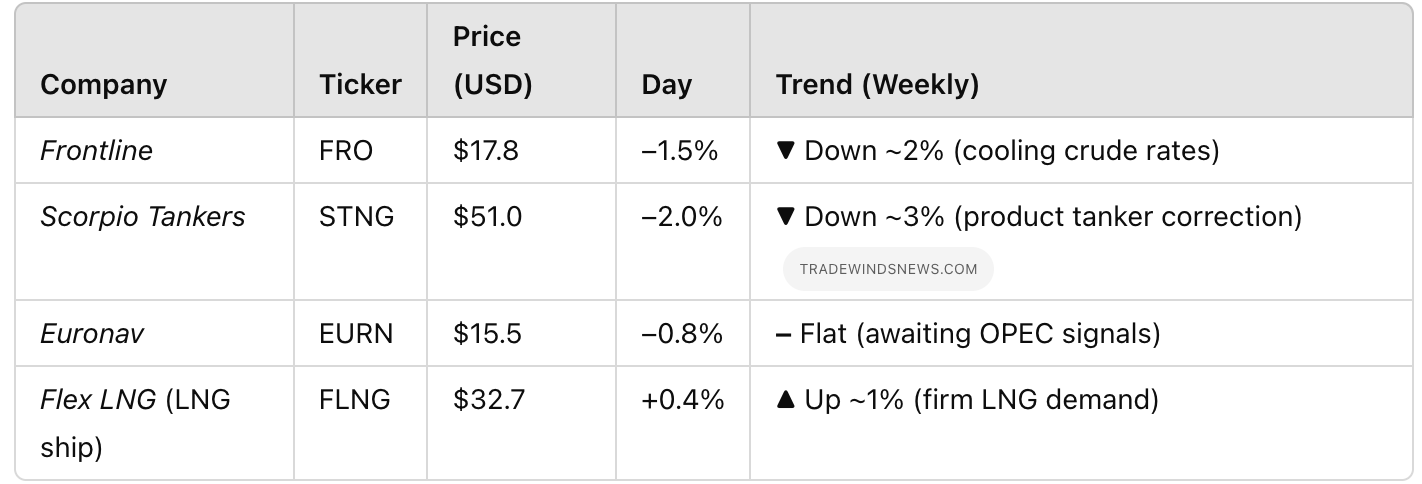

Liquid Bulk (Tankers & LNG) (oil, product, and gas shippers)

Insight: Tanker equities retreated with broader markets. Product tanker owners fell after a recent rally (e.g. Scorpio –2% today) (Rally aborted: Most shipping stocks back in red after broader market ...). However, LNG carrier stocks are stable to positive, tracking rising gas demand into 2025. Overall, investors remain bullish on tankers’ tight supply, but near-term volatility is driven by oil price swings and geopolitics.

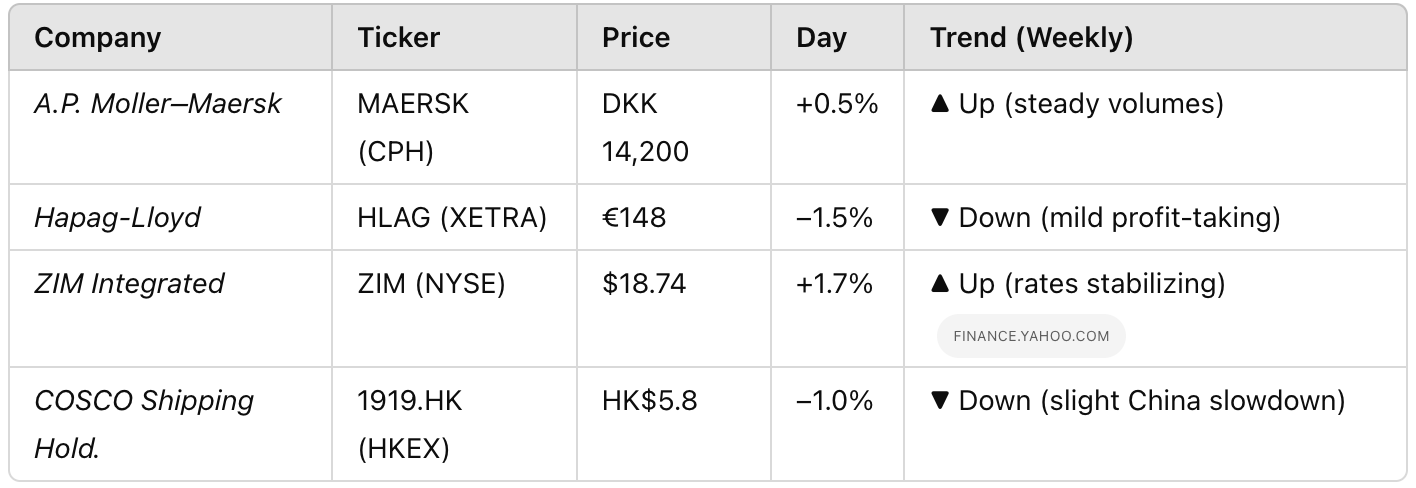

Container Lines (global container shipping operators)

Insight: Container shipping stocks are mixed. ZIM rose +1.7% today, bouncing on improved rate outlook (ZIM Integrated Shipping Services Ltd. (ZIM) Stock Historical Prices ...). Maersk and Hapag-Lloyd trade near flat this week – volumes are strong but freight rates have normalized from last year’s highs. Investors are watching alliance reshuffles and cost-cutting for future earnings direction.

Market observers note that shipping shares broadly outperformed the market earlier this year, but are now selectively moving as sector fundamentals diverge. Dry bulk shares trend up on commodities demand, tankers remain near multi-year highs despite short-term dips, and container lines are navigating a soft landing from peak profits.

Venture Funding News

The maritime and transport tech space is steaming ahead with fresh capital injections:

$100M Maritime Tech Fund: Singapore-based Motion Ventures launched a $100 million fund dedicated to maritime technology – the largest sector-focused VC fund to date (Motion Ventures launches largest-ever maritime tech fund at $100M to meet the industry’s new pace of adoption | Sustainable Logistics International). Backed by 17 industry heavyweights, “Fund II” will invest in ~25 startups aiming to digitize and decarbonize shipping, with check sizes from $250k up to $10M (Motion Ventures launches largest-ever maritime tech fund at $100M to meet the industry’s new pace of adoption | Sustainable Logistics International). This massive war chest underscores investor confidence in innovations for green fuels, smarter routing, and port efficiency.

Battery Systems Startup Scales: Echandia, a Swedish maritime battery supplier, secured SEK 220 million (~$20.6M) to expand production (Echandia reveals $20.6M funding to 'boost' sustainable operations). The funding round – led by Alantra’s energy transition fund and Industrifonden – will boost Echandia’s manufacturing in Sweden and a new U.S. facility (Echandia reveals $20.6M funding to 'boost' sustainable operations). The capital supports larger electrification projects, as Echandia’s battery systems help cut vessel emissions and fuel costs by enabling electric and hybrid ships (Echandia reveals $20.6M funding to 'boost' sustainable operations).

AI Logistics Platform: U.K.-based startup Loadar raised $4M seed funding to expand its AI-driven freight procurement platform to the U.S. (Loadar secures $4M to fuel US expansion and tackle $9T logistics market — TFN). The tool automates how large shippers source and manage carriers, targeting inefficiencies in the $9T logistics market. The round, led by Frontline Ventures, will help double Loadar’s team and bring its software to more enterprise clients seeking to streamline shipping operations (Loadar secures $4M to fuel US expansion and tackle $9T logistics market — TFN).

(Echandia reveals $20.6M funding to 'boost' sustainable operations) Example of sustainable maritime tech: a modular battery system by Echandia, used to electrify ships. Green tech solutions like this attracted significant venture funding in recent deals (Echandia reveals $20.6M funding to 'boost' sustainable operations) (Echandia reveals $20.6M funding to 'boost' sustainable operations).

Green & Autonomous Tech: PitchBook data shows a surge in funding for clean shipping and autonomy. Wind propulsion and efficiency startups (e.g. auxiliary sail providers) have collectively raised tens of millions – e.g., Norsepower’s €28M round to deploy rotor sails (Norsepower secures €28 million from investors to bring sails back to ...). Meanwhile, autonomous vessel tech firms and AI routing startups (like Orca AI, Shone) are drawing new investments as industry players seek safer, more efficient ops.

Private Equity & Ports: PE firms are also active – e.g., a $100M+ infrastructure round for a “smart port” technology fund was announced in Asia, aiming to modernize port automation and supply chain software (sources like PitchBook report increased dealflow in port management solutions). Additionally, first-of-a-kind vessels are getting backing: Switch Maritime raised ~$15M to build hydrogen-fueled ferries, and Trafigura’s ammonia-fueled ships order (see Key Players section) reflects capital being directed into low-carbon vessels.

Overall, maritime innovation funding is at an all-time high. Industry insiders note that decarbonization goals and supply chain disruptions have catalyzed venture interest in everything from alternative fuels to logistics AI. Expect to see new startups and collaborations bridging tech and shipping throughout 2025, as this traditionally conservative sector embraces digital transformation.

Deep Dive into Key Players

Maersk: Fleet & Green Strategy – A.P. Møller–Maersk is leveraging its massive scale to push green shipping and end-to-end logistics. Fleet Expansion: Maersk is in the midst of a generational fleet renewal – it has 18 large dual-fuel methanol container ships on order for delivery by 2024–25 (Maersk names first large methanol container ship). The first 16,200 TEU methanol-fueled vessel, Ane Maersk, entered service in 2024, pioneering carbon-neutral fuel use. Maersk even completed its first retrofit of an existing ship to run on methanol (Maersk retrofits its first container ship to methanol - WorldCargo News). These moves align with Maersk’s target to achieve net-zero emissions by 2040. In terms of capacity, Maersk’s operating fleet remains robust (~4.1 million TEU, second globally to MSC), and it has strategically moderated capacity growth to support freight rates post-pandemic.

Green Strategy: Maersk leads in alternative fuels – not only methanol, but also exploring ammonia and biofuel blends. It has conducted biofuel trial voyages and calls for global carbon pricing to incentivize cleaner shipping. The company is also part of the First Movers Coalition, committing to zero-carbon vessels. Market Positioning: Maersk is transforming from a pure carrier to an integrated logistics powerhouse. After acquiring logistics firms (warehousing, e-commerce fulfillment, etc.), nearly half of Maersk’s revenue now comes from landside logistics services. This diversification helps smooth out volatile ocean earnings. On the ocean side, Maersk and Germany’s Hapag-Lloyd have forged the new “Gemini” operational alliance starting Feb 2025, pooling ~290 vessels (3.4M TEU) on major East-West trades (Maersk and Hapag-Lloyd are entering into an operational cooperation). This replaces the 2M Alliance with MSC (ending next year) and is intended to improve service reliability for customers. Maersk’s dual strategy – invest in green ships and broaden end-to-end services – keeps it a pivotal player shaping industry trends. As evidence of its financial clout, Maersk is funding these expansions largely from its record profits earned during the 2021–22 freight boom, while still returning cash to shareholders via dividends and buybacks.

Major Commodity Traders (Trafigura, Glencore, etc.): These trading giants play a behind-the-scenes but critical role in global shipping. Trafigura, for instance, is one of the world’s largest vessel charterers, arranging over 5,000 voyages per year hauling oil, metals, and minerals (Shipping and marine logistics | Trafigura) (Shipping and marine logistics | Trafigura). Traders like Trafigura and Glencore do not own all the commodities they ship – they act as middlemen, using their fleets to move cargoes from producers to consumers wherever arbitrage opportunities arise. This means they heavily utilize the spot freight market and time charters. Trafigura currently controls a modern fleet (owned and chartered) including tankers, bulkers, and gas carriers; it has also invested in new vessels equipped for low-carbon fuels. Notably, Trafigura ordered four ammonia-fueled gas carriers (MGCs) in 2024, which will be capable of using green ammonia as propulsion (Trafigura inks newbuild contract for ammonia-powered gas carriers). It also completed the first-ever ship-to-ship ammonia fuel transfer in early 2025 (First-ever Ammonia and Propane Co-loaded Vessel Completes ...), signalling how traders are driving decarbonization trials (Trafigura performs first ship-to-ship transfer of ammonia). The firm has committed to cut its shipping carbon intensity 25% by 2030 (vs 2019) (Shipping and marine logistics | Trafigura), testing wind-assist sails on tankers and onboard carbon capture.

Glencore, on the other hand, is a mining and trading behemoth heavily involved in dry bulk shipping. It charters large fleets of bulk carriers to transport coal from its mines in Australia/Colombia and grains from its agriculture division. With coal still in demand in Asia, Glencore’s shipments influence the Capesize and Panamax markets. However, as the world shifts, Glencore has pared down some coal assets and is focusing more on metals like copper, cobalt, nickel – critical for batteries. Those metals often move in smaller bulk parcels or containerized form, so Glencore’s logistics span both bulk and container shipping. Other traders like Vitol (oil) and Cargill (grains) are also key players: Cargill is notably the largest charterer of bulk carriers in the world for grains, and has partnered on wind sail trials as well. The commodity traders thus are both power users of shipping and innovators – by optimizing routes and experimenting with technology (Cargill and Trafigura both invest in digital freight platforms), they influence market efficiency.

In terms of freight contracts, traders often secure long-term charters for stability. For example, Trafigura has multi-year charters on dozens of tankers to move crude and refined products globally. They also contract LNG carriers – e.g. Trafigura is supplying LNG to various countries and has term chartered LNG vessels accordingly (KOGAS shortlists BP, Trafigura, Total for 2.1 mil mt/year long-term ...). This ensures commodity flows (like U.S. LNG to Asia, or Middle East LPG to Europe) are underpinned by shipping length fixed by traders.

Capital Flow & Liquidity in Shipping: The shipping sector has seen active financing and M&A, reflecting newfound profitability. Recent investments: Shipowners flush with cash (especially container lines and tankers) are investing in newbuilds and retrofits. Lenders and lessors are keen too – for instance, Chinese leasing companies continue to finance a large share of new ship orders, providing billions in export leases. Banks are cautiously increasing exposure under ESG frameworks (many are in the Poseidon Principles initiative linking loans to decarbonization targets).

One headline example: Trafigura just renewed a $5.6 billion revolving credit facility in March 2025 (Shipping and marine logistics | Trafigura), ensuring ample liquidity for its trading and shipping activities. It also secured a $300M loan from Korea’s KEXIM to guarantee supply of battery metals (Shipping and marine logistics | Trafigura) – indirectly supporting shipments of those commodities. These moves show that capital markets remain open to big traders, which in turn keeps freight moving. On the carrier side, Mergers and acquisitions are reshaping segments: in tankers, the attempted Frontline-Euronav merger fell apart in 2023, but Euronav’s assets have since partially shuffled (some sold to rivals, and a merger with smaller owner International Seaways rumored). Consolidation talk continues, as big owners seek scale – e.g. Atlas Corp (Seaspan) was taken private by investors in 2023 with an eye to ordering more container ships at cheaper rates.

Shipowners are enjoying easier access to credit thanks to strong earnings. For instance, many Greek owners secured new bank loans to order dual-fuel ships. And private equity is still active: 2024 saw PE firm Navium acquire a portfolio of 20 bulk carriers, and alternative lenders like hedge funds finance older vessel acquisitions. Even commodity houses are stepping in – Mercuria and Golden Ocean formed a JV to buy tankers in 2024, indicating creative capital flows.

Additionally, we see record newbuilding investment: The global orderbook swelled as owners contracted new tonnage. In fact, shipbuilders have order backlogs not seen in a decade – container lines ordered hundreds of ships during the boom, and now tanker and gas carrier orders are picking up. Clarkson Research noted over 1,200 new vessels (across all types) were ordered in 2024 amid high cashflows. This influx of new ships (often financed via 5–7 year charter deals or leasebacks) means capital is being plowed back into the industry, though with a lag until delivery. Conversely, ship recycling has been minimal (as charter rates made even old ships profitable), which also means financiers of scrap sales (often local cash buyers) have been less active.

Key takeaway: The shipping industry is awash in liquidity from the recent boom. Companies are using the capital for fleet renewal, greener tech, and strategic deals. Lenders remain supportive – evidenced by major credit lines like Trafigura’s multi-billion facilities (Shipping and marine logistics | Trafigura) (Shipping and marine logistics | Trafigura) – and new funding mechanisms (like sustainability-linked loans, green bonds for shipping) are emerging. This capital flow will shape fleet composition and ownership in the coming years, keeping the sector dynamic.

Major Shipping Lanes & Trade Flows

Singapore Shipping Watch: The world’s top transshipment hub continues to see heavy traffic. Singapore’s port handled a record 41.12 million TEU last year ( Singapore's maritime industry sets new highs in 2024-Xinhua ), and 90% of it was transshipment (containers swapped between ships) – highlighting its pivotal role linking trade lanes. Transshipment trends: Cargo volumes through Singapore are rising as carriers reroute shipments to avoid other disruptions (e.g. many Asia-Europe services made Singapore an exchange point during the Red Sea crisis). The port’s operators, PSA, even reactivated older berths and yards to handle the surge, increasing weekly capacity to 820k TEU (Singapore's Port Breaks Records in 2024: A Testament to Maritime Excellence - Containerlift.co.uk - Transport/Lifting/Shipping’). As a result, despite global supply chain challenges, Singapore managed to reduce congestion – average container vessel waiting times were kept low through measures like night-time barge ops and optimized scheduling (Singapore's Port Breaks Records in 2024: A Testament to Maritime Excellence - Containerlift.co.uk - Transport/Lifting/Shipping’).

Bunker fuel pricing: Singapore is also the largest bunkering port. Prices for marine fuel have been fluctuating with oil markets. As of today, VLSFO (0.5% sulfur fuel) in Singapore is around $516/ton (Singapore Bunker Prices, Singapore - BUNKER INDEX), up ~1% from yesterday. Over the past week, bunkers ticked upward on tighter supply – fuel inventories are slightly down and demand from recovering traffic is up. By contrast, low-sulfur fuel oil a month ago was closer to $470/ton, so costs have climbed alongside crude oil’s rally. The bunker spread (price difference) between Asia and other regions remains moderate, keeping Singapore fuel competitive. In addition, Singapore saw record alternative fuel sales in 2024 – over 50,000 tons of biofuel blends were bunkered as the industry tests greener options (Singapore's Port Breaks Records in 2024: A Testament to Maritime Excellence - Containerlift.co.uk - Transport/Lifting/Shipping’).

Port congestion: Singapore presently reports minimal congestion. Yard utilization is high but stable, and vessels generally berth on arrival. This is a stark improvement from the pandemic era. Regionally, however, some spillover is monitored – if nearby ports face delays, Singapore can get a wave of diverted calls. As of this week, congestion index for Singapore is ~1.05 (slightly above normal), with minor berth delays mostly due to bad weather last week. Overall, throughput efficiency is excellent, helped by continued expansion at the new Tuas Mega-Port (11 berths open, more coming) (Singapore's Port Breaks Records in 2024: A Testament to Maritime Excellence - Containerlift.co.uk - Transport/Lifting/Shipping’). Bunker queue: Even bunker waits are short – about 80 vessels bunkered daily on average (Singapore's Port Breaks Records in 2024: A Testament to Maritime Excellence - Containerlift.co.uk - Transport/Lifting/Shipping’).

Suez Canal Watch: All eyes are on Suez as it recovers from recent turmoil. The canal is operating below full capacity due to earlier conflict in the region. Currently, about 32 ships per day are transiting Suez (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA) (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA), compared to the usual ~70–75/day before the Gaza war. This ~60% drop in daily transits has persisted since late 2023 (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA). However, there’s light ahead: the Suez Canal Authority projects traffic will gradually return to normal by late March 2025 with a full recovery by mid-year, assuming geopolitical stability (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA). Indeed, as a ceasefire holds, more ships are daring the route. Large oil tankers had been avoiding Suez due to security risks, but preparations are underway for their return.

Geopolitical impact: The war-related disruptions (Houthi attacks in the Red Sea) forced many vessels to detour via the Cape of Good Hope in 2024, deeply cutting Suez volumes. Egypt reported canal revenue fell ~60% at one point (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA). In May 2024, only 1,111 ships used Suez vs 2,396 a year earlier, and monthly cargo tonnage through Suez plunged by 68% to 44.9 million tons (Suez Canal revenue drops by almost half due to Red Sea crisis) (Suez Canal revenue drops by almost half due to Red Sea crisis). This revenue loss pushed the SCA to extend hefty toll discounts to entice traffic back (Suez Canal revenue drops by almost half due to Red Sea crisis). Now, with security improving, those diversions are slowly reversing. As of February 2025, Suez was handling less than half its normal traffic and earning 40% of normal revenue (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA). The expectation is that by end of Q2 2025, transit counts will be near pre-crisis levels (assuming no new flare-ups) (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA).

Potential delays: Right now, northbound convoys are limited – some ships wait 1–2 days for a convoy slot. Certain high-risk vessel types (VLCCs loaded with crude) still prefer the long route around Africa. SCA is actively reassuring shipowners and providing armed escorts. If tensions fully ease, we could see a sudden influx of deferred ships. The upside: more transits would restore Suez’s typical share of global trade (~10% by tonnage, ~22% of container trade) (Traffic in Suez Canal is expected to normalize by March - SAFETY4SEA). The downside: a flood of rerouted ships might briefly congest Port Said or Suez anchorages when they come back. The canal has capacity for ~90 ships/day, so it can absorb the return, but careful scheduling will be key.

Panama Canal Watch: The Panama Canal faces a very different challenge – water levels. A severe drought through 2023 led to unprecedented draft restrictions and cut transits. By late 2024, rains improved slightly, but capacity is still constrained. In January 2025, Panama Canal transits averaged 32.6 ships per day (total 1,011 that month) (Transits through Panama Canal fell in January for first time in almost a year | Reuters). This was the first monthly drop in almost a year, down from 34+ ships/day in Dec. Even though 36 transit slots were available daily, not all could be filled due to earlier backlog and caution (Transits through Panama Canal fell in January for first time in almost a year | Reuters) (Transits through Panama Canal fell in January for first time in almost a year | Reuters). Water levels: Gatun Lake, the canal’s reservoir, remains below optimal. The ACP (Panama Canal Authority) has kept draft limits in place – currently ~47.5 feet for Neopanamax locks, forcing some larger bulkers and tankers to lighten loads. The good news: 2024’s El Niño drought conditions have started to abate slightly, and rainfall in early 2025 has been closer to normal. This should gradually ease draft limits in coming months.

Waiting times: Last year saw vessels queuing for over 10 days in the worst period. Now in March 2025, wait times are much improved but still 2–3 days on average for ships without reservations. The Canal Authority has prioritized certain vessels (like LNG carriers and cruise ships) for booking to reduce economic impact. In February, the canal offered 36 slots/day but demand only filled ~32 on some days due to the draft restrictions (some shippers opted to reroute via Suez or Cape) (Transits through Panama Canal fell in January for first time in almost a year | Reuters). There is also ongoing impact from toll increases: higher fees have led a few operators to avoid Panama when possible. The canal tolls were restructured starting 2023 – Panama implemented a simplified value-based toll system. Notably, for container ships, the charge on empty containers is being phased up from $2/TEU (2023) to $6/TEU in 2025 (Panama Canal’s Simplified Tolls Structure Approved by Panama’s Cabinet Council - Autoridad del Canal de Panamá) (lower than initially proposed $8/TEU) to incentivize better utilization (Panama Canal’s Simplified Tolls Structure Approved by Panama’s Cabinet Council - Autoridad del Canal de Panamá). Some bulk shippers complained about surcharge hikes, and the U.S. government even sparred with Panama over fees for Navy vessels (Transits through Panama Canal fell in January for first time in almost a year | Reuters) Panama insists these increases are needed for waterway investments.

Toll adjustments: In the fiscal year ending Sep 2024, Panama Canal’s toll revenue fell 5% to $3.18 billion due to reduced traffic from the drought (Transits through Panama Canal fell in January for first time in almost a year | Reuters). Previously, between 2020 and 2023, revenues had jumped 26% to $3.35b as trade rebounded and tolls rose (Transits through Panama Canal fell in January for first time in almost a year | Reuters). To balance finances, the ACP is sticking with its approved toll hikes (gradual annual rises through 2025 across segments) (Panama Canal’s Simplified Tolls Structure Approved by Panama’s Cabinet Council - Autoridad del Canal de Panamá). For instance, besides empty box fees, the loyalty program discounts for frequent container lines are being phased out by 2025 (Panama Canal’s Simplified Tolls Structure Approved by Panama’s Cabinet Council - Autoridad del Canal de Panamá). Also, booking fees were raised – e.g., Super category vessels now pay $50,000 vs $41,000 for a prime booking slot (Trump-Panama tiff highlights rising transit cost | Latest Market News). These higher costs have opened arbitrage for alternate routes; indeed some low-priority, less time-sensitive shipments (like certain bulk cargoes) have chosen to go around Cape Horn to save on tolls, especially when canal wait times made overall transit comparable (Transits through Panama Canal fell in January for first time in almost a year | Reuters).

In summary, the Panama Canal is navigating a tricky period of water shortages and pricing tweaks. Traffic is down about 10% in tonnage terms compared to a year ago (Sep-Jan period) (Transits through the Panama Canal still down 10% - BIMCO). The canal authority is hopeful that normal rainfall in the wet season will restore capacity. They are also pursuing long-term solutions – a proposed $2 billion water management system (possibly new reservoirs) to ensure future reliability (The Panama Canal Is Running Out of Water. Thousands May Be ...). Shippers are watching closely; any sign of relief (or further drought) will swing certain trade routes.

Key lane status:

Panama – gradually recovering, but for now some Asia-US cargo is moving via Suez or intermodal US rail as alternate. LNG and grains shippers, in particular, have hedged with alternate plans until drafts fully normalize.

Suez – improving security situation means likely rapid recovery in Q2; carriers plan to reintroduce Suez routings for Asia-Europe as insurance costs drop.

Arctic routes – not a major factor currently (seasonal and experimental), but of interest if traditional lanes are constrained. 2025’s Arctic winter was harsh, so no Northern Sea Route traffic in Q1.

Both canals are vital chokepoints, and 2025 has illustrated how climate and conflict can disrupt them – leading to significant rerouting, higher costs, and delays in global trade flows.

Commodities & Arbitrage

Global commodity trade drives much of shipping demand, and shifts in these flows create arbitrage opportunities across oceans:

Iron Ore: The steel-making staple is moving in stable volumes from mines to mills. Australia and Brazil remain the top exporters to China, which imports ~1 billion tons/year. So far in 2025, Chinese steel demand is lukewarm (property sector still weak), keeping iron ore futures range-bound (Baltic Index Down on Lower Capesize Rates | Hellenic Shipping News Worldwide). Capesize bulk carriers (180,000 DWT) have seen only modest upticks in fixing rates, as ore volume growth is flat. However, an interesting arbitrage: increased Chinese steel exports to distant markets are indirectly supporting ore demand (Dry Bulk Market Poised for 2025 Upturn, Drewry Says) – China is importing high-grade ore, exporting finished steel, which means longer haul trade (ore in, steel out). For example, Chinese steel heading to Europe or Southeast Asia effectively “carries” iron content twice over the sea. Any stimulus in China could boost ore imports sharply, tightening Capesize supply. Presently, the major miners (Rio Tinto, BHP, Vale) are shipping near full capacity, so the arbitrage for shipowners is if Chinese buyers switch between Brazilian and Australian ore. In recent weeks, Brazil-China freight rates rose relative to Australia-China, suggesting Chinese mills took more Brazilian ore (perhaps for quality or pricing reasons), which is a ton-mile increase benefiting Capesize earnings.

Coal: Global coal flows are undergoing shifts as some regions phase down coal while others ramp up. Europe’s thermal coal imports have dropped after a 2022 spike (with more renewables and gas stabilizing), but Asia’s demand remains high, especially in India, China, and Southeast Asia. Thermal coal: Indonesia is exporting record volumes to meet South and Southeast Asian demand. India also sources more from Russia now at discount. Meanwhile, Panamax coal trades (e.g. US or S.Africa to Europe) are weaker – BIMCO forecasts weaker coal shipments in 2025 globally (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News). That hits Panamaxes especially (coal is >50% of Panamax cargo). Indeed, forward freight agreements indicate softer Panamax rates later this year tied to coal decline. Coking coal: Australia resumed exports to China after a diplomatic thaw, so there’s arbitrage as Chinese buyers switch from US/Mongolian coal back to Australian. This has boosted Supramax and Panamax employment in the Pacific. Arbitrage note: High European natural gas prices in past years caused an arbitrage where U.S. coal went to Europe (long haul) while Russia sent more coal to Asia – that dynamic is now unwinding as Europe uses less Russian coal entirely. Coal arbitrage now is more about quality and price diffs: e.g., if high-grade Australian coal is cheap enough relative to Indonesian, Indian utilities might take Aussie coal despite distance – benefitting Capes/Panamaxes. With China’s informal ban on Australian coal lifted, some Capes are doing Queensland to China again, a route that had been dormant – this is effectively arbitrage in action, displacing shorter-haul ASEAN coal.

Oil: Crude oil trade routes have been radically redrawn since 2022, creating plentiful arbitrage for tankers. Western sanctions on Russia forced Russian crude exports to shift from short Baltic->Europe routes to long Baltic->India/China voyages. As a result, tanker ton-miles exploded – by one estimate, diversions around Africa (avoiding Suez) added 200,000 barrels/day in extra fuel consumption and 4.5% higher ship emissions in 2024 (Global Maritime Industry Year in Review | Proceedings - March 2025 Vol. 151/2/1,465). Russian Urals crude has been selling at discount, so traders arbitrage it by shipping to Asia for refining. This means Aframax and Suezmax tankers that once did 1-week Baltic-NWEurope runs now do 4-week trips to India, tying up vessel supply. The arbitrage persists as long as Russian crude is cheaper than Middle Eastern or African crude in those markets. Conversely, Europe is now buying more Middle East crude and U.S. oil. So we have a triangle: US Gulf -> Europe flows up (utilizing many Aframax/LR2 and VLCC via reverse lightering), Middle East -> Europe increased, and Middle East -> Asia slightly reduced (some ME oil was reallocated to Europe). All of this inefficiency benefits tankers. Product oil (diesel, gasoline): Arbitrage is also rife. Europe banned Russian diesel, so Russia sends diesel to Latin America/Africa, while Europe imports diesel from the Middle East, India, and the U.S. This has kept product tankers busy on long voyages. Recently, a diesel arbitrage window opened where U.S. Gulf diesel, which was oversupplied, flowed to Europe as prices there rose – a fleet of MR tankers set sail, narrowing the price gap. Similarly, when Asian gasoline is cheap, traders book tankers to ship it to the Americas. These arbitrages appear and disappear with relative prices, often month by month, providing short-term boosts to freight rates in those lanes.

LNG: The liquefied natural gas trade has become highly elastic, responding to price differentials between Asia and Europe. In the winters of 2022–24, Europe paid premium prices to attract LNG away from Asia (due to the gas crisis). By winter 2024–25, Europe’s storage was relatively full, and Asian demand (especially from China, Japan) rebounded, causing Asian LNG prices to rise above European prices – reopening the arbitrage for Atlantic cargoes to head East (LNG prices in Asia rise again allowing for arbitrage opportunities | Global LNG Hub). Indeed, as of Q1 2025, JKM (Asia) LNG price exceeded the TTF (Europe) price sufficiently to justify U.S. Gulf Coast cargoes diverting to Asia (LNG prices in Asia rise again allowing for arbitrage opportunities | Global LNG Hub). This arbitrage is significant: an LNG carrier from the U.S. to Europe might take ~11 days, whereas to Asia via Panama ~ twenty-plus days. If Asia pays more, traders will send the ship the longer route to capture the spread. We saw multiple U.S. LNG cargoes in Feb/March re-route mid-voyage toward Asia as that price gap widened. However, constraints: The Panama Canal’s restrictions meant many LNG carriers had to take the longer Suez or Cape route, adding even more ton-miles (LNG prices in Asia rise again allowing for arbitrage opportunities | Global LNG Hub). This added cost, but with Asian prices so high, it was still profitable – and it tightened shipping, driving spot LNG freight rates up. Now, as Europe will need to refill gas storage by summer, competition with Asia will heat up (Europe to intensify LNG competition with Asia to meet 2025 storage ...). Analysts predict Europe must attract ~10% more LNG in 2025, so if Asian demand stays strong, price-driven tug-of-war will continue. This creates volatility in LNG shipping: when arbitrage favors Asia, ships take longer voyages (good for utilization); if Europe outbids Asia, voyages shorten. LNG traders (like Shell, Trafigura, Gunvor) actively play this arbitrage, timing cargo destinations to market signals. For shipowners, this means periods of higher spot rates and repositioning voyages. Notably, the US is ramping LNG output with new terminals (e.g. Calcasieu Pass online, etc.), which will flood the Atlantic with cargoes looking for the best netbacks – potentially ease the competition somewhat if supply increases (US LNG production ramp-up likely to help ease summer competition ...). But weather (a cold snap or heatwave) can swing prices and re-route dozens of ships, demonstrating how LNG has become a truly global, arbitrage-driven trade.

Grains: Agricultural flows have been disrupted by conflict and weather, opening new trade routes. The ongoing war in Ukraine severely curtailed Black Sea grain exports. In 2023–24, Ukraine’s grain exports fell and became intermittently constrained by corridor agreements. As a result, grain importers in the Middle East and Africa turned to other suppliers – notably the U.S., Brazil, and Argentina for corn and wheat. This created an arbitrage: for example, Egypt traditionally bought Ukrainian/Russian wheat (short haul); with Ukrainian supply unreliable, Egypt bought more European and U.S. wheat. U.S. Gulf wheat to Egypt is a much longer haul (Panamax via Atlantic) – benefiting freight. Similarly, Asia (like China) started buying Brazilian corn for the first time in large volume in 2023 after politics limited U.S. corn. Brazil’s huge corn harvests provided an arbitrage – Chinese buyers found Brazilian corn cheaper than U.S., so they booked Panamax and Supramax bulkers from Santos to China. Those voyages (South Atlantic to Far East) are very long, tightening vessel supply. As of 2025, China continues to import Brazilian corn and even sorghum, especially after approving Brazilian sorghum imports (Dry Bulk Market Poised for 2025 Upturn, Drewry Says), reducing reliance on U.S. supplies. This is a structural shift that adds ton-miles. Meanwhile, Brazil had a record soybean crop in 2024, with massive exports to China. Brazil’s soy exports have expanded so much that the U.S. – normally China’s top Q4 supplier – faced competition. Chinese crushers arbitraged by maxing out on cheaper Brazilian beans even off-season, which meant some U.S. Gulf beans looked for other markets (like Europe). This dynamic swings freight: when Brazil exports more to Asia, Cape and Panamax demand from Brazil soars (as seen last year, Brazil’s soybean exports were up ~15%). If Argentina’s crop rebounds in 2025 (after drought), it could further shift soy trade patterns. Black Sea grain: Russia has continued large exports (record wheat exports in 2024), but mainly to Middle East/North Africa. The trade is happening but on a “gray fleet” of smaller, often older ships (due to high war risk insurance). Freight rates ex-Black Sea are heavily discounted with risk premiums. If peace were to break out, a flood of Ukrainian grain could hit the market – grain freight from Black Sea would spike, and likely displace some U.S./EU shipments. Until then, arbitrage for non-Black Sea producers stays open – e.g., Poland and Romania have been trucking some Ukrainian grain to their ports to export, and the EU had to manage internal gluts. The upshot for global shipping: longer routes have partially replaced short Black Sea routes, which means more demand for ships on, say, the Brazil-China or U.S.-Nigeria grain routes.

Emerging arbitrage opportunities: The market is always hunting for the next play. In dry bulk, one emerging arbitrage is nickel ore and bauxite flows: Indonesia’s ore export ban pushed China to import bauxite from Guinea (farther) and nickel matte from elsewhere – that’s creating new long-haul trades. In containers, surprisingly, arbitrage can matter too – e.g., as vessel space becomes abundant, some savvy forwarders engage in “triangulation” routing: shipping goods via alternate ports where rates are lower. One example: Chinese exporters sending cargo via Singapore or Malaysia to take advantage of cheaper backhaul rates – effectively an arbitrage of freight costs. This is niche but shows how rate differentials even create routing detours in container shipping.

Also, empty container repositioning could be seen as arbitrage: with so many empty containers needing to move from West to East, some carriers are now offering discounts to load empties with low-grade commodities (scrap, recyclables) that otherwise wouldn’t move – turning an empty repo into a paying cargo trip. This has spurred trades like shipping plastic scrap or wastepaper from US/EU to Asia at very low rates, utilizing capacity that would be empty.

Lastly, environmental regulations might create a new arbitrage: the IMO 2020 sulfur cap already created the HSFO vs VLSFO fuel price arb (some ships installed scrubbers to profit by burning cheaper HSFO). In 2025, with FuelEU and carbon costs in Europe, there may be a “carbon arbitrage” – e.g., a shipowner might prefer to load cargo in a non-EU port to avoid EU carbon fees and then deliver to the EU by feeder, if that avoids cost. We could see some cargo routing shifts (perhaps more transshipment just outside EU) to arbitrage these new costs – though this is just beginning and closely watched by regulators.

In summary, commodity flows in 2025 are characterized by longer distances and shifting partners. Arbitrage – whether due to price, sanctions, or policy – has generally increased ton-miles, which is bullish for shipping demand. Ship operators and traders who can flexibly reroute are capitalizing on these opportunities, keeping the global fleet busy and freight rates relatively supported despite plenty of new ships.

Expert Opinions & Policy Insights

Industry experts and analysts weigh in on the current trends and regulatory changes shaping shipping:

BIMCO’s Market Outlook: Shipping association BIMCO notes a cautious bulk market ahead. In its January analysis, BIMCO projected that dry bulk demand might fall 0.5–1.5% in 2025 (main scenario) even as fleet supply grows ~2-3% (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News). This imbalance could pressure freight rates compared to 2024. Specifically, BIMCO warns that if Red Sea routes fully reopen mid-2025, it will shorten distances and especially hit Panamax demand (given expected weaker coal volumes). They foresee Panamax rates potentially dropping disproportionately, while Capesizes could be more resilient due to very low fleet growth (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News). In the interim, BIMCO observed that in January the BDI was down 36% year-on-year (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News) due to seasonal factors (early Lunar New Year) and a 2% YoY drop in cargo loadings. They expect a rebound in Q2 as seasonal grain exports and ore restocking pick up, but overall 2025 bulk rates are anticipated lower than 2024 on an annualized basis (BIMCO Dry Bulk Market Report: Return to the Red Sea would weaken market - India Shipping News). For containers, BIMCO has commented that the continued delivery of new mega-ships and weak demand growth (~3-4% in 2025) could keep pressure on freight rates, though a wave of scrappings or slower steaming might tighten supply. In tankers, BIMCO sees a relatively balanced outlook – their latest tanker report suggests crude tanker demand will “tighten slightly” in 2025 with ton-mile support from dislocated trade (BIMCO: Crude Tanker Shipping Market To Tighten Slightly in 2025 ...), while fleet growth remains manageable (~1-2%). Overall, BIMCO’s tone is that of cautious optimism tempered by oversupply concerns in some sectors.

Drewry’s Analysis: Maritime research firm Drewry offers a slightly more upbeat take for certain segments. According to Drewry’s forecasts, the dry bulk sector is poised for stronger earnings in 2025 driven by two factors: sustained commodity demand in select areas and the impact of environmental regulations effectively curbing supply. Drewry highlights coal and grain trades as surprisingly resilient – for example, European coal demand may be down, but Asia’s coal and China’s grain imports remain robust. They also point out that while China’s domestic construction is sluggish, Chinese steel exports (to distant regions) could “provide a silver lining” by generating additional shipping demand. Indeed, Drewry notes China has started importing sorghum from Brazil (a new trade) and that any European economic stimulus (like ECB rate cuts) could revive steel and cement imports to Europe (Dry Bulk Market Poised for 2025 Upturn, Drewry Says). On the supply side, new IMO/EU environmental rules – such as the IMO Carbon Intensity Indicator (CII) and the EU’s FuelEU Maritime – are causing ships to slow down or retrofit, effectively reducing available capacity. Drewry expects this slower steaming and higher fuel cost environment to support freight rates (fewer active ships), and thus they are relatively bullish on earnings upside for bulk carriers in late 2025 (Dry Bulk Market Poised for 2025 Upturn, Drewry Says). In containers, Drewry has noted that freight rates have “found a new normal” above pre-pandemic levels (Drewry suggests new normal for higher global container rates). While they foresee softer rates in 2025 compared to the boom, they believe carriers’ discipline (idling and cancellations) will prevent a complete rate collapse. Notably, Drewry’s recent Financial Health Check 2025 for container lines showed carriers are still profitable and that contract rates for 2025 may settle only ~15% below 2024 on key routes – manageable given cost reductions. One caveat Drewry raises is the potential U.S.–China trade tension around the U.S. presidential transition: they warned early 2025 could see disrupted flows (e.g. tariffs affecting soybean routes) (Dry Bulk Market Poised for 2025 Upturn, Drewry Says). So far, no major new tariffs have hit, but it’s a scenario on the radar.

Regulatory Changes: A wave of new regulations is breaking over the industry. As of January 1, 2025, the EU’s FuelEU Maritime regulation took effect, requiring gradual reductions in greenhouse gas intensity of fuels used by ships calling at EU ports (Dry Bulk Market Poised for 2025 Upturn, Drewry Says). This, along with the inclusion of shipping in the EU Emissions Trading System (with phase-in starting 2024), is expected to drive up voyage costs on EU routes. Experts say in the short term the cost impact is modest – FuelEU targets a 2% emissions reduction by 2025 which many can meet with current fuel blends – but long term it forces adoption of biofuels, e-fuels or other tech. The International Maritime Organization (IMO) also revised its GHG strategy in mid-2023, aiming for net-zero emissions “by or around 2050” and interim checkpoints (like -20% CO₂ by 2030). This will likely bring stricter global measures. Already, IMO’s EEXI and CII rules (efficiency and carbon intensity indexing) enforced since 2023 are pushing older, less efficient ships to slow steam or retrofit. One consequence noted by industry observers: the charter market is fragmenting – charterers are starting to prefer vessels with better CII ratings (A or B), effectively pricing out some ships with a ‘D/E’ rating (Dry Bulk Market Poised for 2025 Upturn, Drewry Says). This “green segmentation” could affect vessel earnings. A BIMCO official recently commented that some charters now include clauses penalizing poor CII performance.

Analyst Insights – Clarksons Research reports that global shipping is in the midst of its strongest multi-year earnings since 2008, but predicts a rebalancing. They project overall fleet growth of ~3% in 2025 against trade volume growth ~2-3%, which could loosen fundamentals. However, Clarksons also notes the fleet orderbook as a % of fleet is only ~10% for tankers and bulkers (very low by historic standards), meaning after the current delivery wave in containers, the supply side looks quite restrained – a positive sign longer term. Lloyd’s List economists have flagged macro risks: higher interest rates and slowing GDP could temper cargo growth. Yet, the IMF’s latest outlook (as cited by some industry reports) actually raised 2025 GDP slightly, which could mean upside for seaborne trade.

Industry leaders’ views: The CEO of Maersk recently emphasized that reliability and decarbonization are the top priorities – hinting that shippers (cargo owners) are now demanding greener shipping and more consistent schedules over just low prices. Similarly, BIMCO’s new president, Šarika (the first woman in that role), opined that regulatory clarity will spur investment in new green ships, but urged governments to support fuel infrastructure. Meanwhile, at a recent Drewry webinar, analysts suggested that if freight markets soften, carriers might form more vessel-sharing alliances or mergers (especially in the struggling feeder and regional carrier arena). Intertanko (tanker owners association) has advocated for pragmatic timelines on emissions rules, arguing the tech (like ammonia engines) isn’t fully ready – an insight into policy debates.

On the policy front, we also see port state initiatives: e.g., California started enforcing a stricter low-NOx requirement for vessels hoteling (2025 onwards), and the IMO is discussing a potential global fuel levy or GHG fund (proposal to charge ~$100/ton CO₂) – which if implemented could drastically alter fuel economics. Major maritime nations are split on this, but momentum is growing after MEPC80.

Lastly, experts at DNB Markets and Goldman Sachs shipping desks believe 2025 could be a transition year where the narrative shifts from cyclical peak to environmental upgrade cycle. They advise keeping an eye on scrap prices (if steel prices rise, more old ships might scrap, tightening supply) and on orderbook composition – 2025–26 deliveries are heavily skewed to containers and LNG carriers, with relatively few crude tankers or bulkers coming, which could set those latter segments up for a run if demand surprises to the upside.

In summary, the consensus from experts: short-term caution, long-term transition. Markets are normalizing after an extraordinary run, but the fundamentals remain fairly healthy. And above all, decarbonization policy is the wild card that will shape investment and operations for years to come – a point everyone from BIMCO to Drewry to Maersk’s CEO agrees on. As one analyst quipped, “The shipping cycles of old are now entwined with the carbon cycle” – meaning economic and environmental pressures must be managed together.

Trivia – Shipping Fact of the Day

Did you know? The longest ship ever built was the supertanker Seawise Giant (later known as Knock Nevis). It measured 458.5 meters (1,504 feet) in length – longer than the Empire State Building is tall – and had a full load draft of 24.6 m (Knock Nevis: the largest ship ever built). Fully laden, it could not fit through the Suez or Panama Canals or even the English Channel due to its massive size (Knock Nevis: the largest ship ever built). This ULCC could carry 4.1 million barrels of oil in one voyage (Knock Nevis: the largest ship ever built). Interestingly, the ship was sunk during the Iran-Iraq War in the 1980s, then salvaged and returned to service, only to end its days as a floating storage unit before being scrapped in 2010. The Seawise Giant remains a legend – a true behemoth of the seas that holds the record as the heaviest and largest self-propelled ship in history. It even took 5.5 miles for it to come to a full stop from top speed and about 2 miles to turn around (Knock Nevis: the largest ship ever built). A testament to human engineering, no ship of greater length has ever been constructed since!

That’s all for today’s edition of Daily Maritime Pulse. Here’s wishing you fair winds and following seas! 🚢🌏

Disclaimer:

This newsletter Sagisu Shipping ("Daily Maritime Pulse") is provided strictly for informational purposes and should not be interpreted as financial or investment advice. The views, opinions, news, and analyses presented herein reflect current market conditions and industry insights and are subject to change without notice. Readers should always perform their own due diligence, seek independent advice from financial professionals, and carefully evaluate their own financial circumstances before making investment decisions.

The authors, editors, or affiliated individuals of this publication may hold direct or indirect equity exposure or other financial interests in the companies and industries discussed. Therefore, there may be a potential conflict of interest regarding any business or security mentioned. This newsletter neither recommends nor endorses the buying or selling of specific securities or financial instruments.